Home / Current Affairs

Mercantile Law

Procedural Requirements in GST Appeals

« »29-Nov-2025

Source: Allahabad High Court

Why in News?

Justice Piyush Agrawal of the Allahabad High Court in the case of M/s Sun Glass Works Private Limited v. State of U.P. and 2 Others (2025) quashed an appellate order passed by the Additional Commissioner on grounds of procedural irregularity, where judgment was reserved and delivered without proper notice to the petitioner.

What was the Background of M/s Sun Glass Works Private Limited v. State of U.P. and 2 Others (2025) Case?

- The petitioner, M/s Sun Glass Works Private Limited, is a Private Limited Company engaged in manufacturing and sales of glass bottles.

- During March 2021, the petitioner purchased various types of chemicals as raw materials for manufacturing glass bottles from registered dealers who issued proper tax invoices.

- On 17 February 2022, a show cause notice was issued under Section 74(1) of the GST Act alleging that Input Tax Credit had been availed by fraud or mis-statement.

- The petitioner submitted a detailed reply along with supporting documents including copies of tax invoices, bank statements, and Form GSTR 2-A.

- On 10 May 2022, the assessing authority passed an order demanding tax and penalty without providing a copy of the alleged survey report or opportunity of hearing to the petitioner.

- Aggrieved by the order dated 10 May 2022, the petitioner filed an appeal before the Additional Commissioner, Grade-2 (Appeals), Mainpuri.

- On 18 September 2024, the appellate authority fixed a hearing date, during which the judgment was reserved.

- The judgment was subsequently delivered on 25 September 2024, dismissing the appeal, but the petitioner was not given notice of this date.

- The petitioner challenged both the original order dated 10 May 2022 and the appellate order dated 25 September 2024 through a writ petition.

What were the Court's Observations?

- The Court noted that the petitioner's counsel argued there is no provision in the GST Act permitting the practice of reserving judgment and delivering it on a later date without notice to the parties.

- The petitioner relied on the precedent established in M/s Wonder Enterprises v. Additional Commissioner, Grade-2 & Another, decided on 12 September 2024.

- The Additional Commissioner filed a personal affidavit pursuant to the Court's order, but failed to mention any provision or notification empowering the authority to pass judgment on a date other than the hearing date without issuing notice or providing opportunity to be heard.

- The Court held that the issue was squarely covered by the judgment in M/s Wonder Enterprises case.

- The Court observed that in view of the peculiar facts and circumstances, the impugned order dated 25 September 2024 could not be sustained in the eyes of law.

- The Court emphasized that the matter required reconsideration with proper adherence to procedural requirements.

- The impugned order dated 25 September 2024 passed by the Additional Commissioner, Grade-2 (Appeals), Mainpuri was quashed.

- The writ petition was allowed, and the matter was remanded back to the Additional Commissioner for deciding the issue de novo.

- The Court directed that the appellate authority must grant due opportunity of hearing to all stakeholders.

- The Court ordered expeditious disposal, preferably within three months from the date of production of a certified copy of the order.

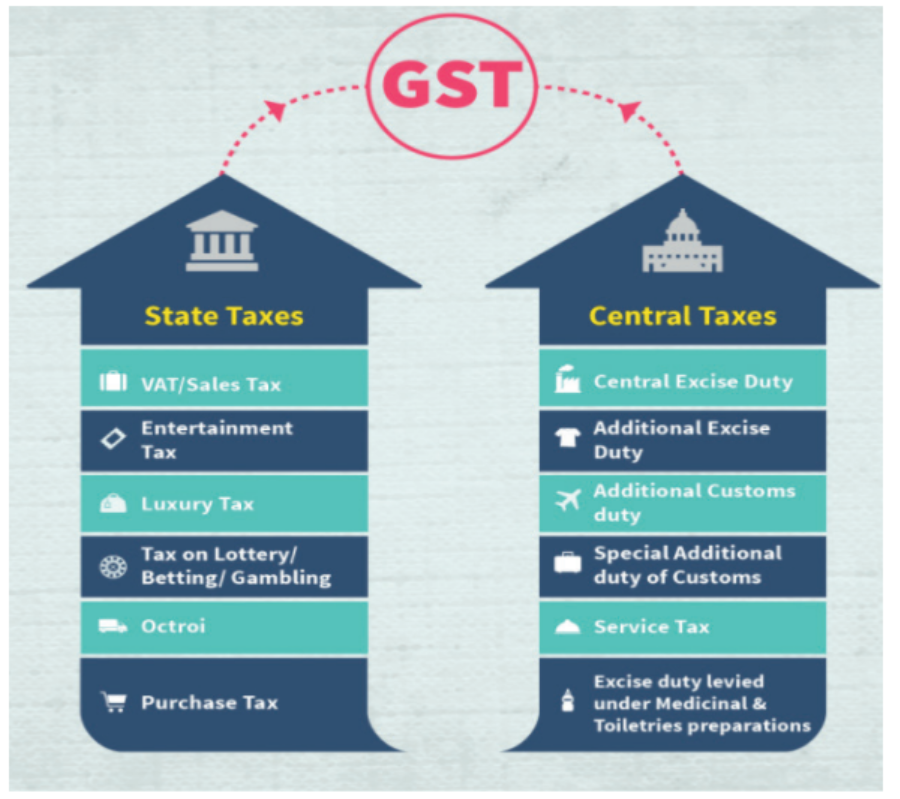

What is the Goods and Services Tax (GST) Act, 2017?

About:

- Introduced by the 101st Constitutional Amendment Act, 2017, is a comprehensive indirect tax levied on the supply of goods and services in India.

- It is a value-added tax (VAT) that replaced multiple indirect taxes previously levied by the Centre and States.

Key Features:

- Dual GST Structure: Includes Central GST (CGST) and State GST (SGST); Integrated GST (IGST) is applicable for inter-state transactions.

- GST Council: It is the primary body for GST policymaking and rate decisions.

- The GST Council is a joint forum of the Centre and the states.

- It was set up by the President as per Article 279A (1) of the amended Constitution.

- Members:

- The members of the Council include the Union Finance Minister (chairperson), the Union Minister of State (Finance) from the Centre.

- Each state can nominate a minister in-charge of finance or taxation or any other minister as a member.

- Functions:

- The Council, according to Article 279, is meant to “make recommendations to the Union and the states on important issues related to GST, like the goods and services that may be subjected or exempted from GST, model GST Laws”

- Goods and Services Tax Network (GSTN): help taxpayers in India to prepare, file returns, make payments of indirect tax liabilities and do other compliances.

- Threshold Exemption: Small businesses with turnover below a certain limit are exempt from GST. This makes compliance easier and protects micro enterprises from excessive paperwork.