List of Current Affairs

Home / List of Current Affairs

Civil Law

No Entitlement to Dual Dearness Allowances

17-Mar-2026

Why in News?

Justice C Kumarappan of the Madras High Court, in P Vanajakshi v. The Metropolitan Transport Corporation and Others (2026), dismissed a writ petition filed by a woman who sought dearness allowance on her regular pension in addition to the dearness allowance she was already receiving on her family pension.

- The Court held that the concept of dearness allowance is grounded in the effect of inflation upon an individual, and therefore a single person cannot be entitled to two such allowances simultaneously.

What was the Background of P Vanajakshi v. Metropolitan Transport Corporation (2026) Case?

- The petitioner was appointed on April 20, 1974, in the Tamil Nadu State Transport Corporation on compassionate grounds following the death of her husband and was already receiving family pension at the time of her appointment.

- In 2001, she superannuated from the post of Selection Grade Assistant. Her grievance was that although she was in receipt of two pensions — family pension and regular pension — she was not being paid dearness allowance along with her regular pension.

- She accordingly sought directions against the Managing Director of the Metropolitan Transport Corporation and the Administrator of the Tamil Nadu Transport Corporations Employees Pension Fund Trust for payment of dearness allowance along with her regular pension.

- The Trust opposed the petition, submitting that since the petitioner had opted for commutation of pension, a sum of Rs. 862 was deducted from her monthly pension and the remaining amount of Rs. 2,995 was being paid along with dearness allowance.

- The Trust further contended that the petition was filed on a misconception of facts and sought its dismissal.

What were the Court's Observations?

- On the Principle of Dearness Allowance: The Court observed that the concept of dearness allowance is premised upon the impact of inflation on an individual employee. Since the petitioner was already receiving dearness allowance on her family pension, granting an additional dearness allowance on her regular pension would result in one individual receiving two separate dearness allowances — a position inconsistent with the foundational principle underlying the allowance.

- On Rule 20A of the Tamil Nadu State Transport Corporation Employees' Provident Fund: The Court noted that Rule 20A(ii) provides that a person re-employed after retiring from a pensionable post will be eligible for dearness allowance on any one of their pension amounts. While the Rule may not be directly applicable to the petitioner's case — since her appointment was on compassionate grounds rather than re-employment in the strict sense — the Court held that the underlying principle, namely that a single individual cannot receive two dearness allowances, was fully applicable.

- On the Facts of the Case: On perusing the counter affidavit filed by the Trust, the Court found that the petitioner was, in fact, already receiving her regular pension along with dearness allowance from 2001 onwards. The Court agreed with the respondent authorities that the petition had been filed without adequately accounting for the commutation of pension, and accordingly dismissed it.

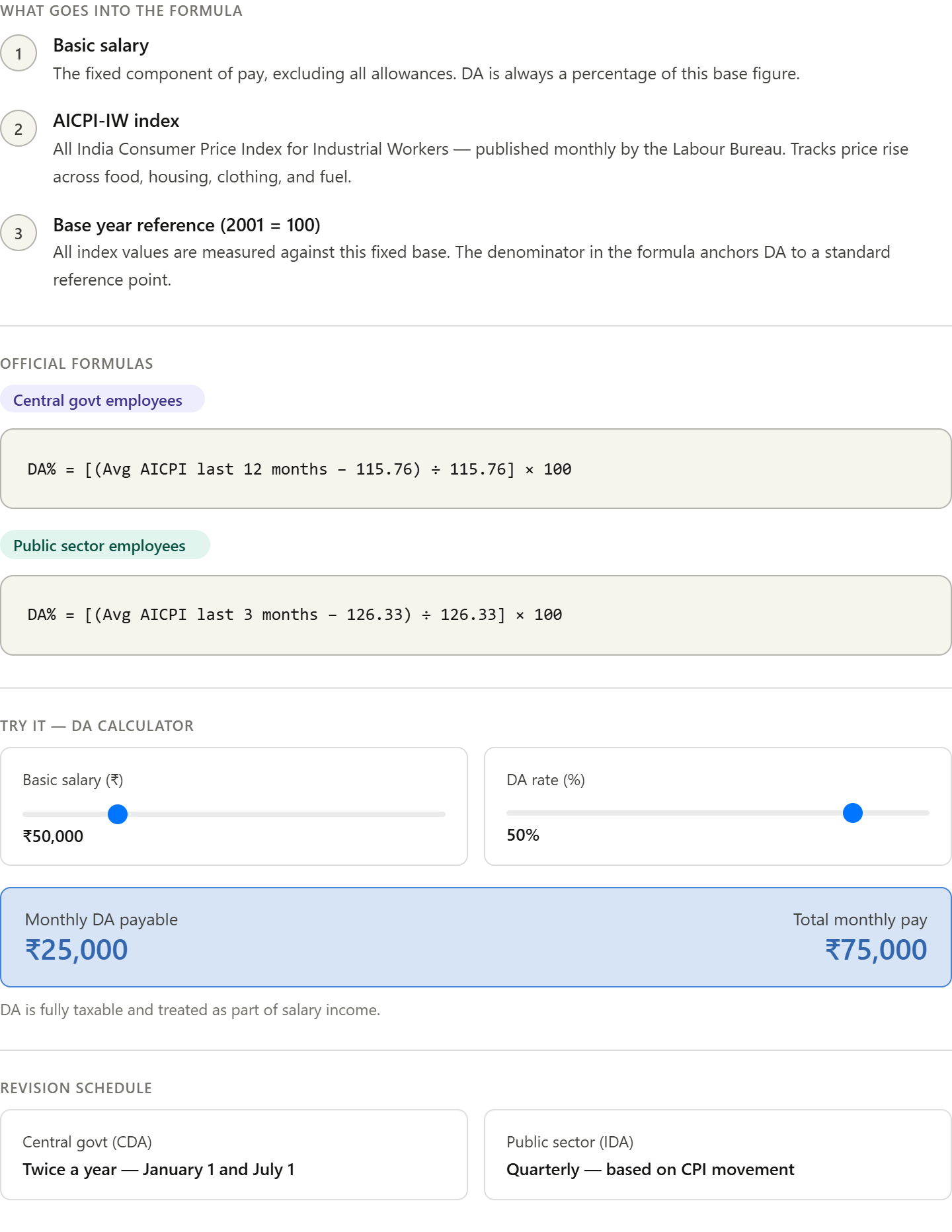

What is Dearness Allowance?

About:

- Dearness Allowance (DA) is a cost-of-living adjustment paid by the Government and public sector undertakings to their employees and pensioners.

- It is calculated as a percentage of the basic salary or pension and is revised periodically — typically every six months — based on movements in the Consumer Price Index (CPI). Its core purpose is to offset the erosive effects of inflation on the real income of employees and pensioners.

Background and Nature:

- DA is given to employees in India, typically in the government sector, as well as some private sector companies, to help them cope with the rising cost of living due to inflation.

- It is intended to offset the impact of inflation on the purchasing power of employees' salaries and to ensure that their real income remains constant or does not decline.

- The dearness allowance is determined by the location of the employee since the impact of inflation differs — depending on whether a person works in the urban, semi-urban, or rural sector, their DA fluctuates.

- DA is distinct from the basic pay of an employee and is revised separately from salary adjustments.

- DA is fully taxable under the Income Tax Act in India and is treated as part of salary income.

Calculation of DA:

Types of Dearness Allowance:

1. Industrial Dearness Allowance (IDA):

- Applies to employees working in public sector enterprises and government-owned corporations.

- The IDA for public sector employees undergoes quarterly revision depending on the Consumer Price Index to help offset the impact of rising levels of inflation.

2. Variable Dearness Allowance (VDA):

- Applies to employees in specific industries, particularly labour-intensive sectors under the central government.

- Dependent on three components: (i) Base Index — remains fixed for a particular period; (ii) Consumer Price Index — changes every month; (iii) Variable DA amount fixed by the Government, which remains fixed unless the government revises the basic minimum wages.

3. Central Dearness Allowance (CDA):

- Applies to central government employees.

- Revised periodically by the Central Government based on changes in CPI for Industrial Workers.

4. State Dearness Allowance (SDA):

- Applies to state government employees.

- Revised by respective state governments based on changes in CPI or other factors.

5. Dearness Relief (DR):

- Provided to pensioners to compensate for the impact of inflation on their pensions.

- Pensioners typically receive the same percentage of DA as current employees.

- Called Dearness Relief (DR) when provided to pensioners.

6. City Compensatory Allowance (CCA):

- Sometimes considered a type of DA.

- Provided to employees working in metropolitan cities or high-cost areas to offset the higher cost of living.

Impact on Pensioners:

- DA is also provided to pensioners — called Dearness Relief (DR) — to compensate for the impact of inflation on their pensions.

- Since DA compensates for the effect of inflation on one individual's cost of living, a person drawing multiple pensions is entitled to DA on only one pension at a time.

Significance:

- Protects government employees and pensioners from the erosive effects of inflation.

- Ensures that real income and purchasing power do not decline over time.

- Provides a structured, index-linked mechanism for periodic revision of compensation.

- Accounts for regional variation — urban, semi-urban, and rural employees may receive different DA rates based on local cost-of-living conditions.

DA vs. HRA:

Constitutional Law

Air Force Group Insurance Society Is 'State' U/A 12 of the COI

17-Mar-2026

Source: Supreme Court

Why in News?

A bench of Justices Sanjay Karol and Vipul M. Pancholi of the Supreme Court, in Ravi Khokhar & Ors. v. Union of India & Ors. (2026), overturned the Delhi High Court's decision and held that the Air Force Group Insurance Society (AFGIS) is a 'State' within the meaning of Article 12 of the Constitution of India.

- The Court held that AFGIS performs a public function intrinsically linked to the State's duty toward armed forces personnel, and that the deep governmental involvement in its administration and finances brings it squarely within the definition of an instrumentality of the State.

What was the Background of Ravi Khokhar & Ors. v. Union of India & Ors. (2026) Case?

- The Air Force Group Insurance Society is a welfare and insurance body serving members of the Indian Air Force.

- In December 2016, the Board of Trustees of AFGIS resolved to revise employees' pay scales in accordance with the Sixth Central Pay Commission recommendations.

- Subsequently, in a meeting held on February 13, 2017, the Board reversed its earlier decision and resolved to delink the Society's pay structures from Central Government pay scales entirely.

- Employees were issued a notice on May 22, 2017, asking them to accept the revised service conditions.

- Aggrieved by this reversal, the employees challenged the decision before the Delhi High Court by way of writ petitions under Article 226 of the Constitution.

- The Delhi High Court dismissed the petitions, holding that AFGIS was a self-contained welfare and insurance scheme funded by member contributions and therefore did not qualify as 'State' under Article 12. Consequently, it ruled the writ petitions to be not maintainable.

- The employees appealed to the Supreme Court against this dismissal.

What were the Court's Observations?

On the Public Function Test:

- The Court held that AFGIS undeniably performs a public duty. It reasoned that the protection and welfare of armed forces personnel is a core government function, given that the role of the armed forces is directly tied to the sovereignty and security of the nation.

- The Court observed that members of the armed forces are required to operate under strict rules and at times in the most severe and adverse circumstances, making the provision of insurance coverage a public function — one that addresses a collective obligation the State owes to a defined class of persons whose service is indispensable.

On Deep and Pervasive Control:

The Court noted several significant factors pointing to deep governmental involvement in the functioning of AFGIS, including:

- The Society was established with the sanction of the President of India, who also specifically approved its deputation rules.

- The Principal Director of AFGIS is required to brief the Assistant Chief of Air Staff on a monthly basis regarding the Society's cash flow, ensuring continuous monitoring by a senior IAF officer.

- Membership of AFGIS and the consequent deductions from salary are compulsory for every serving IAF officer — there is no individual choice in the matter, as it is a mandate from the employer.

On Administrative Control:

- The Court observed that all members of the Board of Trustees as well as the Managing Committee are serving officers of the Indian Air Force, deputed to AFGIS for fixed tenures.

- In essence, the administration of the body is entirely in the hands of government servants, even though the body itself is structured as a purportedly private, self-contained society.

On the Governing Legal Test:

- Referring to established precedents on the scope of Article 12, the Court reiterated that the cumulative effect of all relevant factors must be assessed to determine whether a body is financially, functionally, and administratively dominated by the State.

- The Court stated that the test is not limited to questions of ownership or origin but is instead informed by accountability, the rule of law, and the practical realities of governance.

On Relief:

- The Court allowed the appeal, set aside the Delhi High Court's order, and held AFGIS to be a 'State' under Article 12 of the Constitution.

- It directed the High Court to decide the writ petitions filed by the appellants expeditiously, bearing in mind that the petitions had been pending since 2017.

What is Article 12 of Constitution of India?

About:

- Article 12 lays down that unless the context otherwise requires, the State includes the Government and Parliament of India and the Government and the Legislature of each of the States and all local or other authorities within the territory of India or under the control of the Government of India.

- The definition of State is inclusive and provides that State includes the following:

- Government and Parliament of India i.e., the Executive and Legislature of the Union.

- Government and Legislature of each State i.e., the Executive and Legislature of the various States of India.

- All local or other authorities within the territory of India, or under the control of the Government of India.

Local or Other Authorities Within the Territory of India:

- The expression local authorities is defined in Section 3(31) of the General Clause Act, 1897 as local Authority shall mean a municipal committee, district board, body of commissioner or other authority legally entitled to or entrusted by the Government within the control or management of a municipal or local fund.

- The expression local authorities usually refer to authorities such as municipalities, District Boards, Panchayats, mining settlement boards, etc. Anybody functioning under the state; owned; controlled and managed by the State and carrying out a public function is a local authority and comes within the definition of the state.

- The term other authorities have nowhere been defined. Therefore, its interpretation has caused a good deal of difficulty, and judicial opinion has undergone changes over time.

- The Supreme Court in the case of Union of India v. R.C. Jain (1981) laid down the test for determining which bodies would be considered as a local authority under the definition of State enshrined under Article 12 of the COI. The Court held that if an authority:

- Has a separate legal existence

- Functions in a defined area

- Has the power to raise funds on its own

- Enjoys autonomy i.e., self-rule

- Is entrusted by statute with functions which are usually entrusted to municipalities, then such authorities would come under ‘local authorities’ and hence would be State under Article 12 of the COI.

Whether a Body falls Under Article 12 or Not?

- In R.D Shetty v. Airport Authority of India (1979) Justice P.N Bhagwati gave 5 Point test. This is a test to determine whether a body is an agency or instrumentality of the State and goes as follows –

- Financial resources of the State, where the State is the chief funding source i.e. the entire share capital is held by the government.

- Deep and pervasive control of the State.

- The functional character being Governmental in its essence, meaning thereby that its functions have public importance or are of a governmental character.

- A department of Government transferred to a corporation.

- Enjoys monopoly status which State conferred or is protected by it.

- This was elucidated with the statement that the test is only illustrative and not conclusive in its nature and is to be approached with great care and caution.

Case Laws:

- University of Madras v. Shanta Bai (1950), the Madras High Court evolved the principle of ‘ejusdem generis’ i.e., of the like nature. It means that only those authorities are covered under the expression ‘other authorities’ which perform governmental or sovereign functions. Further, it cannot include persons, natural or juristic, for example, Unaided universities.

- Ujjammabai v. the State of UP (1961), the Supreme Court rejected the above restrictive scope and held that the ‘ejusdem generis’ rule could not be resorted to in interpreting other authorities. The bodies named under Article 12 have no common genus running through them and they cannot be placed in one single category on any rational basis.